We’re on Android & iOS Also Now!

To use our app, you need to become a member first. Sign up or log in on our website to unlock the full experience.

To use our app, you need to become a member first. Sign up or log in on our website to unlock the full experience.

Did you know most students can get federal student loans to help pay for college each year? But there are limits on how much you can borrow each year and in total.

Your loan limits depend on whether you're a dependent student or an independent student.

A dependent student still gets support from their parents, so they have to include their parents' financial info on the FAFSA. You are dependent unless you meet one of these:

| Year | Dependent | Independent |

|---|---|---|

| First Year | $5,500max $3,500 subsidized | $9,500max $3,500 subsidized |

| Second Year | $6,500max $4,500 subsidized | $10,500max $4,500 subsidized |

| Third Year & Beyond | $7,500max $5,500 subsidized | $12,500max $5,500 subsidized |

If you go to graduate or professional school (after a bachelor's degree), you can borrow:

But these are only unsubsidized loans (you pay all the interest).

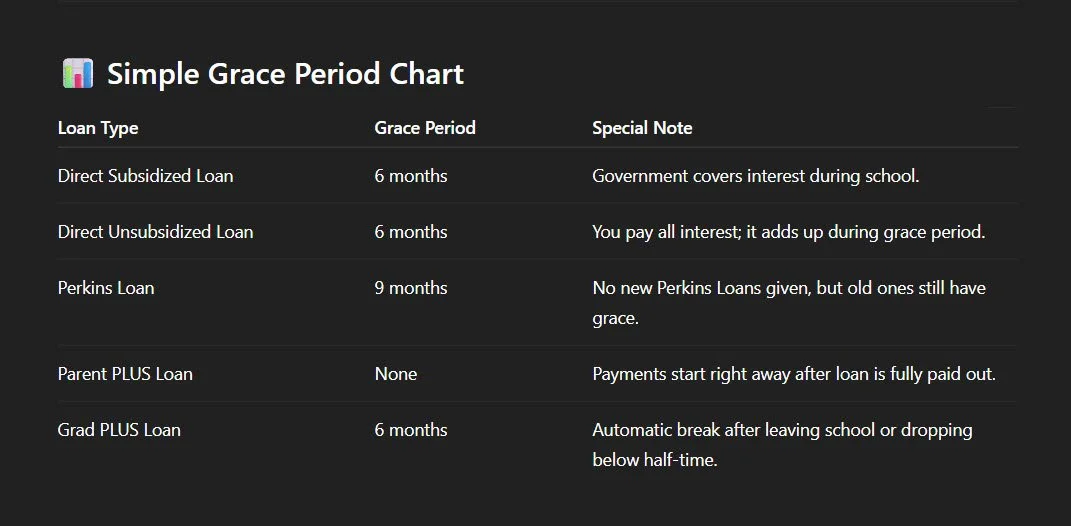

Did you know you don't have to start paying your federal student loans right away after you leave school?

When you graduate, leave school, or drop below half-time enrollment, most federal student loans give you a short "break" called a grace period before you start making payments.

The grace period is meant to give you time to find a job and plan your budget before paying back your loans.

| Loan Type | Grace Period | Notes |

|---|---|---|

| Perkins Loan | 9 months | No new Perkins Loans given, but old ones still have grace. |

| Parent PLUS Loan | None | Payments start right away after loan is fully paid out. |

| Grad PLUS Loan | 6 months | Automatic break after leaving school or dropping below half-time. |

Online now